ATO Sending Letters About Public Reporting Of Company Tax - October 8, 2015

Data: Managing Your Reputational Risk

This week the ATO has sent letters to relevant taxpayers notifying them of their tax information that is to be made public later this year. Taxpayers have until 23 October to check the information and request any corrections.

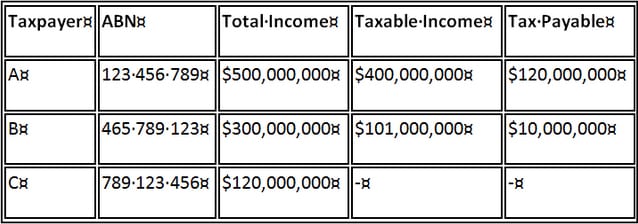

The ATO will be publishing an alphabetical list of corporations with a total income of $100 million or more in their 2013/14 income tax return. The report is expected to look like this.

The information is incomplete. It is open to interpretation. It will be the focus of intense media attention when released in December in an otherwise quiet news period. Effective tax rates will not protect entities from scrutiny. There will be other questions: Is your approach socially responsible? Do you have offshore entities? Why is there such a large discrepancy between total income and tax paid? If corporate tax entities are caught by the measure and are not prepared, their corporate reputation could be at risk.

Tax reputation is now an issue with the potential to affect relationships with a broad range of stakeholders: from customers and employees to investors and the ATO itself. The media is increasingly linking corporate sustainability and social responsibility with tax paying behaviour. For example, Transfield is targeted in the context of the Nauru detention arrangements and arguments that companies relying on government contracts should have best tax practices – Read More. Also targeted is Volkswagen in the context of the recently publicised emissions scandal – Read More.

Corporations who are impacted need to seriously consider their approach to managing the reputational risk posed by the impending disclosure. Experience demonstrates that Tax Directors should not seek to deal with this issue alone. They need to work collaboratively with the CFO/Media Affairs/Investor relations and other interested parties to develop a cohesive and robust strategy. This will require professional expert advice and assistance in a number of areas.

Please contact me for advice and assistance in managing your reputational risk arising from the impending public disclosure of tax information.

October 8, 2015

Disclaimer: The information on this page is for general information purposes only and is not specific to any particular person or situation. There are many factors that may affect your particular circumstances. We advise that you contact Mathews Tax Lawyers before making any decisions.